“This aggression will not stand, man” - The Dude

**If you enjoy this newsletter - do us a favor & forward it to your friends or colleagues**

**Note: we will be writing sporadically, for the indefinite future; if the note is too “hot”, it will only go out via email (will not be available on the site); the aim, at this point, is for a monthly note**

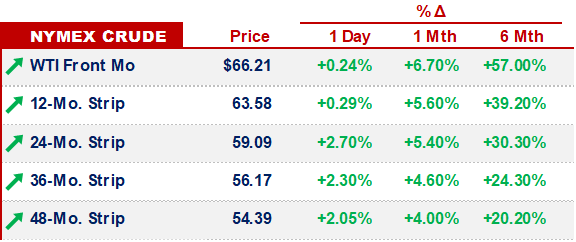

MACRO.

Over the past few weeks, LNG cargos have been rerouted from South Asia to Europe, depriving the former markets of gas. Many crops in Ukraine - the breadbasket of Europe - will not be planted.

The real-world economic consequences of recent economic warfare has only just begun.

The race to fill up gas storage for next winter will result in political & economic turmoil. And when spring turns to summer, we’ll begin to see the fallout in agricultural markets.

While Russia is the target (and will be the biggest loser) in this unprecedented economic war, other economies will also suffer.

Expect riots & price caps.

The lowest bidders (the poorest markets) will likely see orders unfilled.

And note that revolutions often follow lesser events of economic unrest.

In thinking about what may transpire, we’ve found ourselves thinking about the 2nd & 3rd order effects of what may come to pass.

The following interviews & research have either been predictive of recent events or - we believe - have the capacity to be predictive going forward (beyond 1st order effects) -

Research / Data / Commentary:

The artist(s) known as @ViscosityRedux published a comprehensive analysis of the potential energy shortages resulting from recent sanctions

Podcasts:

An interview with Julia Friedlander - a former policy advisor for Europe in the U.S. Treasury Department’s Office of Terrorism and Financial Intelligence - on economic warfare & sanctions; previously, her role at the Treasury was executing sanctions

In an interview from December, Russian-born Dmitri Alperovitch - the former CTO and co-founder of CrowdStrike, the world’s largest cybersecurity company - makes the call that Putin will invade Ukraine

Last week, following the invasion, Dmitri Alperovitch returns to be interviewed on the topic of Russia & Ukraine - and his correct calling of the matter

We’ve thought a lot about a ~90sec tangent in an interview from 2018 with Fabrice Grinda (a former emerging markets tech entrepreneur & venture capitalist) on emerging market risk.

Roughly a decade ago, he the made the call that specific political choices would lead to negative economic outcomes for investments in many emerging market economies.

It has - unfortunately - been a great call -

OTHER NEWS.

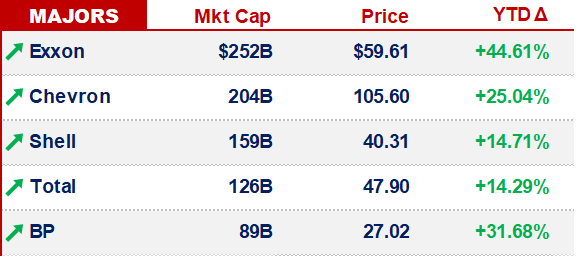

This event will cause prices to inflate, globally (and monetary policy won’t solve it)

A California VC Narrative Violation

We warned a Russian friend of this possibility a couple weeks ago; if you have Russian friends, it may be worth reminding them that many countries in the Americas (especially the US & Canada) were built by people leaving bad situations in Europe

That’s it for now - hope y’all enjoy the rest of your week -

“Strikes and gutters, ups and downs” - The Dude