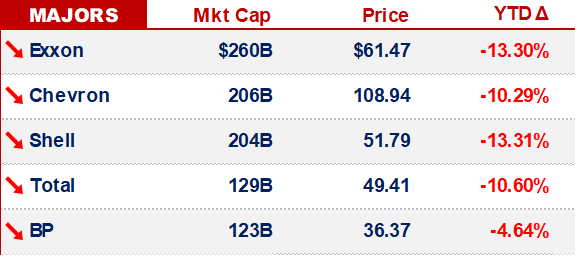

Beyond China

“What are the odds that people will make smart decisions about money if they don't need to make smart decisions - if they can get rich making dumb decisions?” - Michael Lewis - The Big Short

***Editor’s Notes: (1) Matt is in DC this week for a Change of Command ceremony; it’s unlikely that we’ll publish a newsletter on Friday; (2) we decided to send out Tuesday’s newsletter, today - heavy China-focus; (3) the model is updated***

FOLLOWUP.

Two weeks ago, we published a model to attempt to show the speed at which the coronavirus was spreading.

That model was criticized for being dramatic - specifically, overstating the speed at which the virus would spread.

Now that yesterday - the first date that our original model forecasted - has passed, it’s worth considering how the original forecast has held up.

The model’s early forecasts were, in fact, conservative.

**We actually underestimated the near-term risk**

By a factor of 6x.

Reported figures now tally at >40k infections.

Now, back to our critics.

Their error, was an error in base rate.

Every critic who brought substance to their argument (and most did), cited the total number of SARS cases as their base rate:

Both SARS & the Coronavirus 2019-nCoV are coronaviruses that cause respiratory illness

Both viruses appear to indirectly trace back to bats in Wuhan

However, 3x days of official data indicated that this virus was spreading much, much faster than SARS did

We waited for the 4th day of data, before publishing the model.

THE BIG SHORT & BASE RATES.

Using a historical outcome as a base rate can be dangerous.

Especially when the drivers of that outcome include either a (A) significant coefficient or (B) an exponential variable -

We’re reminded of an infamous example of such a miscalculation - the Bill Miller / Steve Eisman panel at DB, in ‘08.

Miller’s argument boiled down to historical outcomes:

“[Bill] Miller pointed out how unlikely it was that Bear Stearns might fail, because thus far, big Wall Street investment banks had failed only after they were caught in criminal activities”

Eisman’s argument went at the drivers (leverage, in that case):

“[Bear Stearns] had $40 in bets on its subprime mortgage bonds for every dollar of capital it held against those bets. The question wasn't how Bear Stearns could possibly fail but how it could possibly survive”

The panel infamously ended with a question from a kid in the audience:

"Mr. Miller," he said. "From the time you started talking, Bear Stearns stock has fallen more than twenty points [45%]. Would you buy more now?”

In the context of Coronavirus 2019-nCoV, the equation of virus reproduction rates is simple. You can add variables into that equation to estimate the effectiveness of quarantines & vaccination dates.

It’s not SARS - it’s math - and, the equation is known.

And you don’t have to trust us - here’s the model.

**Make your own forecast**

Long-story-short, our current forecast is that markets are still underestimating events in China.

Enough so that we bought puts on EM equity indexes -

LIBYA.

The UN is holding talks - in Cairo - attempting to secure an end to the Libyan Civil War.

Talks began yesterday, and an official statement is expected, just before this newsletter is published.

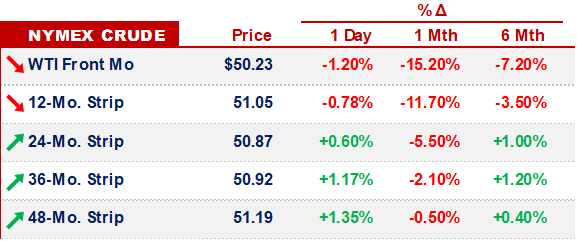

This week begins the 4th week of the Libyan oil blockade.

Crude is down 15% in the last month - in spite of >1MM bopd being taken off the market - by the blockade.

The unfortunate reality is that peace will be bad for crude prices -

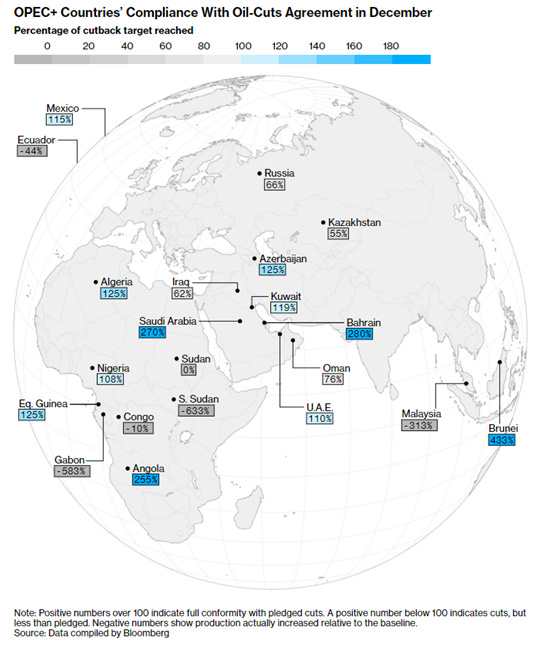

OPEC+ CUTS… ?

As it stands today, OPEC & Russia are unlikely to hold a meeting to discuss production cuts this month, according to Bloomberg.

The planned March meeting will go ahead as scheduled.

Russia has been resisting additional cuts, while Saudi wants to pull back.

We view a lack of action as potential for short-term disaster.

Especially if Libyan oil starts to flow again.

To Russia’s credit - they’re know to be Machiavellian strategists.

They could have a trick up their sleeve.

But this feels like flirting with disaster -

CHINA.

The following are relevant data points & reporting that we’ve found helpful:

Preemptive Central Bank Measures:

“China’s central bank will provide the first batch of special re-lending funds for combating the coronavirus on Monday and will offer the facility weekly to banks later this month. The move comes as the virus outbreak continues to hammer retail spending and industrial production and as economists continue to downgrade their growth forecasts as a result.” - Bloomberg

If Containment Works, it still Hurts:

“The virus’ high infectiousness thus far (relative to SARS) has forced the implementation of far-reaching containment measures”

“Even if these prove successful at containing its spread, they still imply a negative impact on activity, which will be highly concentrated but not limited to China’s first quarter activity.” - Christian Keller, Barlcays

Guangdong Locks Down -

“Guangdong and Shenzhen go into partial lock-down to contain the spread of the illness as the extended Lunar New year holiday ends” - SCMP

Context:

>100MM people live in Guangdong

4th largest Sub-national Economy in the World (after Cali, TX & NY)

Geographically, Guangdong surrounds Hong Kong

Global Supply Chain Issues -

“Three of South Korea’s five car-makers halted their production because they could not get crucial components from their Chinese suppliers” - SCMP

Context:

It’s not just the South Koreans - most Auto players will be affected

If not domestic car manufacturing, then the issue will be auto-parts

On the Rate that the Virus is Spreading:

Data outside of China may be more reliable

If Guangdong does that rate for ~10x weeks, we have a problem

If you’re looking for frequent updates, we recommend Caixin.

We’ll end on a lighter note - on human resilience:

That’s it for today - we’ll most likely be back next Tuesday - enjoy the week -

Disclaimer: none of this is investment advice -